Statrys support always gives prompt and helpful replies. Not only does Statrys offer business solutions but, more importantly, as a client I feel valued.

High-Growth Companies Asia-Pacific 2026

Accounting Services

Awards 2026 for

Integrated ABC Solution

Best Cross-Border Fintech

Payments Platform in

Hong Kong 2025

Best Payments

Solutions 2024

High-Growth Companies Asia-Pacific 2026

Accounting Services

Awards 2026 for

Integrated ABC Solution

Best Cross-Border Fintech

Payments Platform in

Hong Kong 2025

Best Payments

Solutions 2024

A Hong Kong

Business Account

That Just Works

Pay and get paid in multiple currencies

With tools to track and manage every payment — so you stay in control

Say goodbye to the usual friction

100% online application

Apply in minutes, get your business account in a few days. Deliberately fast and easy.

All-in-one Unique in Hong Kong

Add corporate services and accounting alongside your business account. One partner, one login, one team. Simple as ABC.

Real support

Help that doesn’t disappear after onboarding. Get answers from real people when you need them.

Everything you expect

Made simple

1 account supporting

11 currencies

- 1 single account number for all currencies

No more headache when sharing account

details to suppliers.

- 1 single account number for all currencies

- Receive and make payments in all currencies

Helping you scale across borders with ease.

- Receive and make payments in all currencies

- Convert currencies when it suits you

Keep control of your FX costs.

- Convert currencies when it suits you

Local and international

payments, the easy way

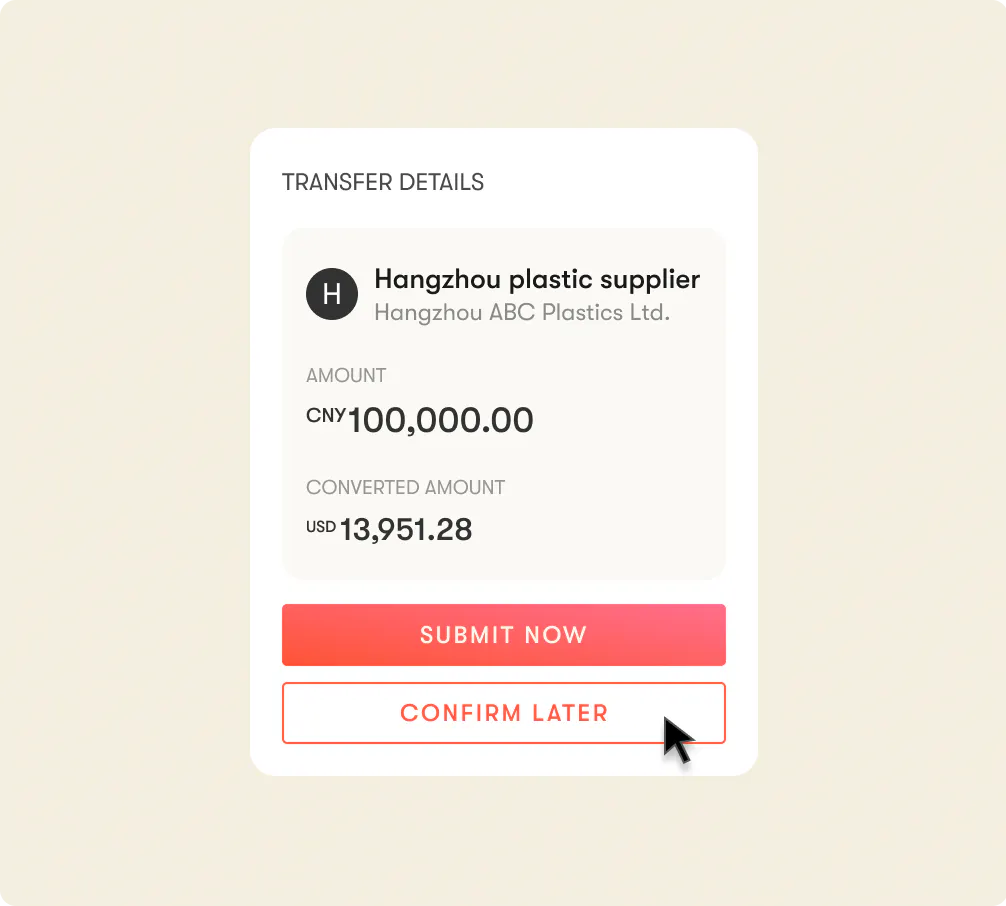

- Pay and get paid across 120+ countries

Connect your business to the world via SWIFT.

- Pay and get paid across 120+ countries

- Local transfers in 13 countries

Pay suppliers in their local currency in minutes, faster and cheaper than SWIFT.

- Local transfers in 13 countries

- Full payment transparency

Track payments in real time and get MT103 anytime.

- Full payment transparency

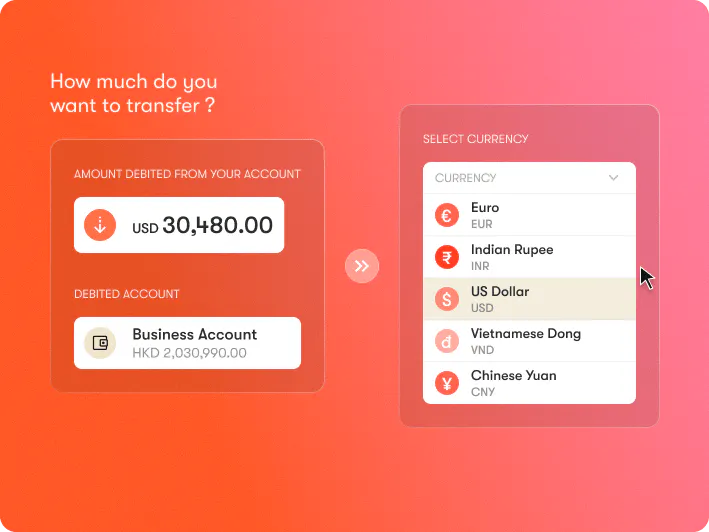

FX rates that work

in your favour

- Rates you can trust

Convert funds based on real-time market rates, refreshed every 60 seconds.

- Rates you can trust

- Keep more of your money

FX fees from 0.1% – save money on every FX transaction.

- Keep more of your money

- Expert support on demand

Dedicated FX specialists when you need guidance.

- Expert support on demand

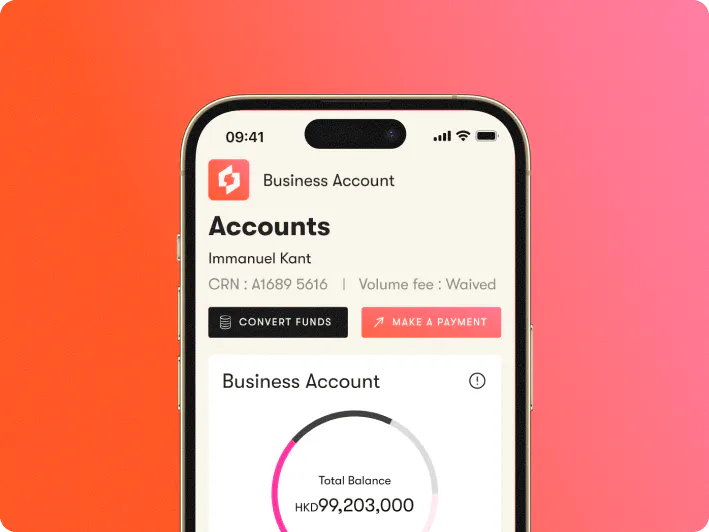

Your account, in your pocket

- Everything at a glance

Check balances and payments in real time.

- Everything at a glance

- Never miss a movement

Instant notifications every time money moves.

- Never miss a movement

- Banking on the go

Convert funds and send payments on the go.

- Banking on the go

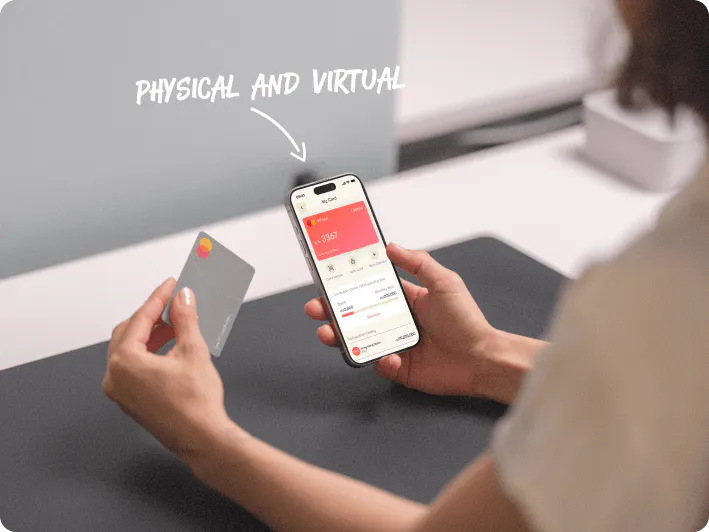

Physical and virtual cards,

built for global business

- Spend worldwide with ease

Use your card online, in stores, and at ATMs anywhere Mastercard® is accepted.

- Spend worldwide with ease

- Stay in control

Freeze, set limits, and manage employee cards in real time.

- Stay in control

- Get your card in minutes

Request your card without paperwork or branch visits.

- Get your card in minutes

The extras that make

a difference included

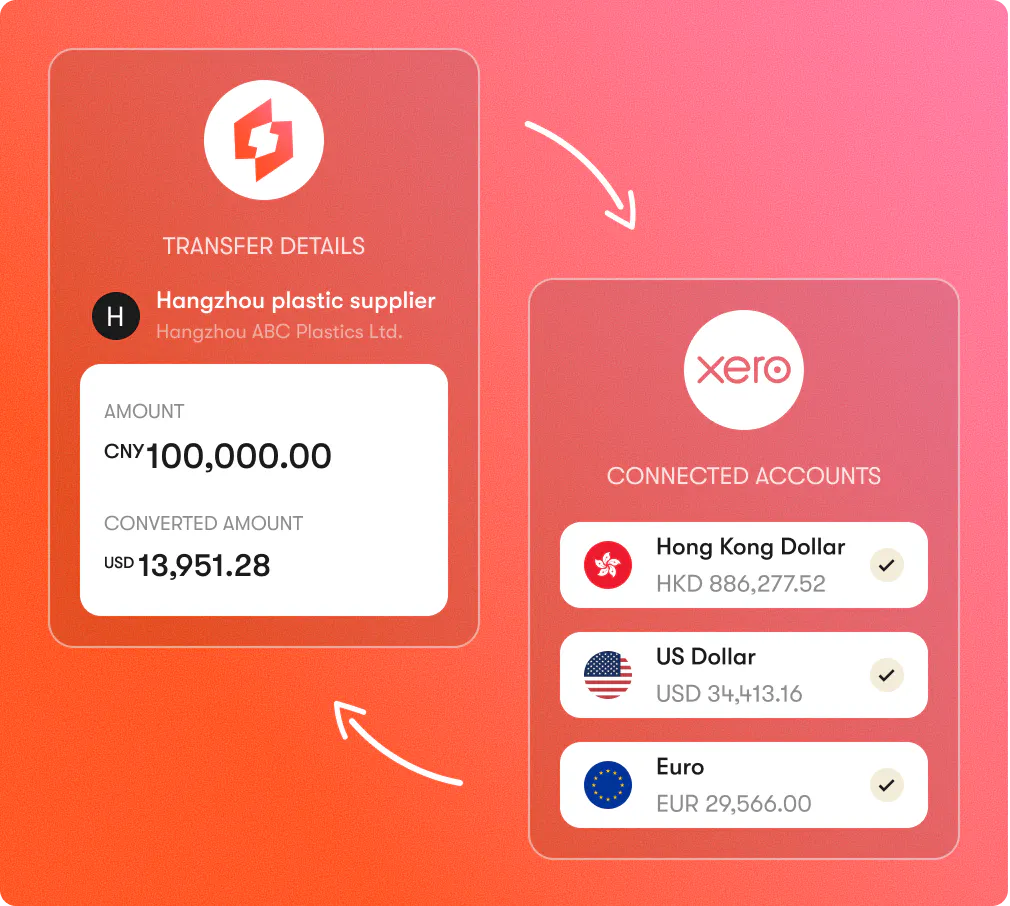

Seamless Xero

integration

Automatically sync all your transactions, including

card payments, to eliminate manual data entry.

Instant reconciliation in multiple currencies

giving you a clear and real-time view of your finances.

Account

Management

Stay in control by assigning clear roles to account

users. Set workflows based on who can view,

initiate, and approve payments.

SWIFT payment

tracking

Get notified of incoming SWIFT payments. Track

outgoing SWIFT payments in real time — and share

this information with your payees.

Integrations to the

digital economy

Centralize your online sales and get paid

worldwide. Easily connect your account to

Shopify, Stripe, PayPal, and your entire digital

ecosystem.

Everything else your business needs, in one place

Open a Statrys account and get access to accounting, corporate services, and more — without switching platforms.

Corporate Services

Handle incorporation, company secretary, and compliance — all from your Statrys dashboard.

Accounting

Transaction-based pricing, IRD-compliant filings, and a dedicated accountant. No surprises.

ABC | All-in-One

Your business account, accounting, and corporate services — bundled, connected, and ready to go.

Approved by

Business owners.

Onboarding was smooth, the fees are fair, and customer support has been consistently helpful. It’s everything you need in a business account—simple, reliable, and well-priced.

Opening a multi-currency account was smoother than expected. The platform is simple and works well for daily business tasks. I also appreciate how quickly the team respond whenever I have a question.

Statrys support always gives prompt and helpful replies. Not only does Statrys offer business solutions but, more importantly, as a client I feel valued.

Onboarding was smooth, the fees are fair, and customer support has been consistently helpful. It’s everything you need in a business account—simple, reliable, and well-priced.

Opening a multi-currency account was smoother than expected. The platform is simple and works well for daily business tasks. I also appreciate how quickly the team respond whenever I have a question.

I’ve been using their service for nearly a year to manage my company in Hong Kong, and it’s been smooth from the start. Everything works efficiently, and the support has been great throughout.

I’ve been using Statrys for 3 years—it’s reliable, transparent, and easy to use. Plus, I’ve saved a lot compared to traditional banks. Works well for my business needs.

We’ve been with Statrys for over a month, and the service has already exceeded expectations. Their team responds within an hour and consistently goes above and beyond to help. We’ve also saved a lot on fees compared to traditional banks in Hong Kong.

I’ve been using their service for nearly a year to manage my company in Hong Kong, and it’s been smooth from the start. Everything works efficiently, and the support has been great throughout.

I’ve been using Statrys for 3 years—it’s reliable, transparent, and easy to use. Plus, I’ve saved a lot compared to traditional banks. Works well for my business needs.

We’ve been with Statrys for over a month, and the service has already exceeded expectations. Their team responds within an hour and consistently goes above and beyond to help. We’ve also saved a lot on fees compared to traditional banks in Hong Kong.

After 6 years with Statrys, I can confidently say it’s one of the best services for SMEs. They’ve been reliable, consistent, and clearly understand what small businesses need. A very good service I continue to trust.

Everything works smoothly, it’s easy to use, and I’ve had no issues at all. I’ve also seen improvements to the platform, including features I personally suggested—which shows they take feedback seriously.

After 6 years with Statrys, I can confidently say it’s one of the best services for SMEs. They’ve been reliable, consistent, and clearly understand what small businesses need. A very good service I continue to trust.

Everything works smoothly, it’s easy to use, and I’ve had no issues at all. I’ve also seen improvements to the platform, including features I personally suggested—which shows they take feedback seriously.

10,000+

SMEs and business owners use Statrys to escape the dark side of admin.

$7B+

Transferred through Statrys. And counting.

1,600+

Companies registered in Hong Kong and Singapore. Still climbing.

$2.5B+

In FX traded, at rates banks can't match.

You’ve got questions

We’ve got answers right here. At least to the most common ones.

Don’t see yours? Ask our Chatbox!

Which industries are prohibited?

We do not provide services or support to customers involved in, operating within, generating income from, or having any direct or indirect dealings in, with, or through the industries listed below.

Please note that this list is provided for illustrative purposes only and is not exhaustive.

- Cryptocurrency, Digital Token, Virtual Asset

- Anonymous or Numbered Accounts, Shell Banking/Companies

- Correspondent Banks

- Crowdfunding

- Cash and Check Handling: Check Cashing, Deposit Taking, Cash Transfer

- Credit repair, Debt Restructuring

- Debt recovery, Debt settlement, Debt Collections

- Multi-level marketing, Financial Pyramid or Ponzi Schemes

- Gambling

- MSBs and PSPs

- Any industry known to be an illegal industry in its local jurisdiction or the UK or HK

- Illegal Drugs and Narcotics Illegal Services

- The sale or distribution of stolen goods, counterfeit goods and violation of intellectual property, or items that violate individual privacy

- Any products harmful to human health (tobacco, e-cigarettes, and e-liquid) and pharmacological goods

- Operating a business that requires a license or special permit without obtaining such license (i.e., Unregulated Auction Houses)

- Production of Adult or Violent content

- Production or Distribution of Offensive Weapons or with potential military applications: Ammunition, Firearms, Explosives, Complex Weapons (i.e., guided missiles), Poison, Nuclear-related

- Psychic services

- Selling, hosting, distributing, producing, or promoting offensive materials, including materials that incites or promotes racial hatred or Discrimination based on gender, race, religion, national origin, physical ability, sexual orientation, or age

- Transactions involving Human Organs and Other Services

- Sanctioned individuals and entities

- Products or services related to political campaigning, social campaigning

- Trading of restricted and/or endangered animal species and products derived from them

- Sales, distribution and/or trade of archaeological and cultural relics

- Import or export of specified ‘dual used goods’ listed on the defense and Strategic Goods List

- Trusts/Funds/Foundations

- Charities, Non Governmental Organisations, Not for Profit Organisations

- Any other businesses or transactions outside of our risk appetite (eg, Oil and Gas related; mining, trading & sales of precious metals such as gold) in accordance with our internal policies, our banking partners’ policies or the policies of participants in our payment network

For the up-to-date list, please visit our FAQ page.

Which countries and regions are not supported by Statrys?

These are the general guidance on jurisdictions that are not supported by Statrys.

In assessing whether Statrys is able to provide business services or facilitate payments, we may consider a range of factors, including, but not limited to:

- Customer location

- Nationality or residency of related parties

- Place of incorporation or registration

- Principal place of business or operations

- Source of funds and wealth

- Origin, routing, or destination of payments

- Any direct or indirect dealings in, with, or through the relevant jurisdictions

- Applicable regulatory, sanctions, or financial crime risks associated with the jurisdictions

The list below is determined based on a range of considerations, including applicable sanctions laws and regulations, our internal risk appetite, and restrictions imposed by our partner financial institutions, among other factors. Please note that the countries and jurisdictions listed are indicative only, are not exhaustive, and may be updated or amended from time to time without prior notice.

- Afghanistan

- Albania

- Belarus

- Bosnia and Herzegovina

- Central African Republic

- Congo

- Cuba

- Ethiopia

- Haiti

- Iran

- Iraq

- Kosovo

- Lebanon

- Libya

- Mali

- Montenegro

- Myanmar

- Nicaragua

- North Korea

- North Macedonia

- Russia

- Serbia

- Sevastopol

- Somalia

- South Sudan

- Sudan and Darfur

- Syria

- Ukraine (Crimea, Donetsk, Luhansk, Kherson, and Zaporizhzhia)

- Venezuela

- Yemen

- Zimbabwe

As a regulated financial institution, Statrys is required to comply with all applicable laws and regulations across relevant jurisdictions. While we endeavour to provide our services as broadly and seamlessly as possible, all business relationships and transactions remain subject to review and assessment on a case-by-case basis in accordance with our risk-based compliance framework and applicable laws and regulations.

For the up-to-date list, please visit our FAQ page.

Can US citizens apply for a Statrys account?

We are unable to accept applications from individuals with the following US affiliations:

- A US Citizen as Director

- A US Citizen as Shareholder/UBO (holding more than 10%)

- A US Resident as Director and/or Shareholder/UBO (holding more than 10%)

What are the restricted countries for the Statrys payment card?

Our payment cards (both virtual and physical) cannot be used in or shipped to any of the following restricted countries based on our agreement with the Payment Card Issuer.

The list below is for indicative purposes only. It is not exhaustive and may be updated by Statrys from time to time:

- Afghanistan

- Albania

- Belarus

- Bosnia and Herzegovina

- Central African Republic

- Congo (The Democratic Republic of)

- Crimea Region Of Ukraine

- Cuba

- Donetsk People’s Republic Region of Ukraine

- Ethiopia

- Iran

- Iraq

- Kherson Republic of Ukraine

- North Korea (Democratic People’s Republic of)

- Kosovo

- Kyrgyzstan

- Lebanon

- Libya

- Luhansk People’s Republic Region of Ukraine

- Mali

- Myanmar

- Nicaragua

- Republic Of Macedonia (The)

- Russia

- Serbia

- Sevastopol

- Somalia

- South Sudan

- Sudan

- Syria

- Tajikistan

- Ukraine

- Venezuela

- Yemen(The Republic of)

- Zaporizhzhia Region Of Ukraine

- Zimbabwe

For the up-to-date list, please visit our FAQ page.

Start with Statrys

Talk to our team

The things you are

probably looking for

If experience tells us anything, your

next move is here.